India Market Outlook 2020

CY 2019 had a lot of action, both on the markets front, as well as policy measures from the government. We had the NDA regime come back to power with a landslide majority allowing it to move forward on policy decisions. The economy though ended the year with sluggishness and a very visible slowdown.

In contrast large cap equities delivered decent returns and debt markets provided spectacular gains for those who were in duration products. INR depreciation was moderate. Either ways it was a positive experience for investors whose allocations were well balanced.

However, the experience was very negative for investors who had significant allocations towards the mid and small cap segment or credit.

We would like to begin the year by providing a perspective of what has transpired, the positives and negatives that await 2020 and our opinion on portfolio positioning along with the key factors that will help change our investment thesis.

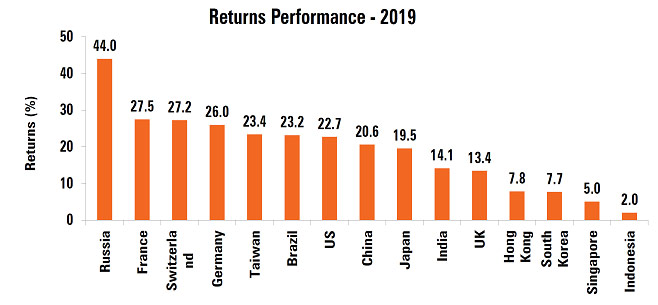

- Within equity markets, the sector and stock gainers have continued to be narrow with a large number of funds underperforming the indices.

- The gainers have been Realty, Energy and Banks. Energy has been dominated by Reliance Industries and Banks are largely led by private sector names that have gained market share due to a defunct public sector.

- The mid and small cap indices continued to underperform.

- There were two key changes to the tax structure.

- Corporate tax was cut to counter the slowdown to 25% from 35% inclusive of surcharge.

- Individual rates of taxes increased for the super rich with enhanced surcharge .

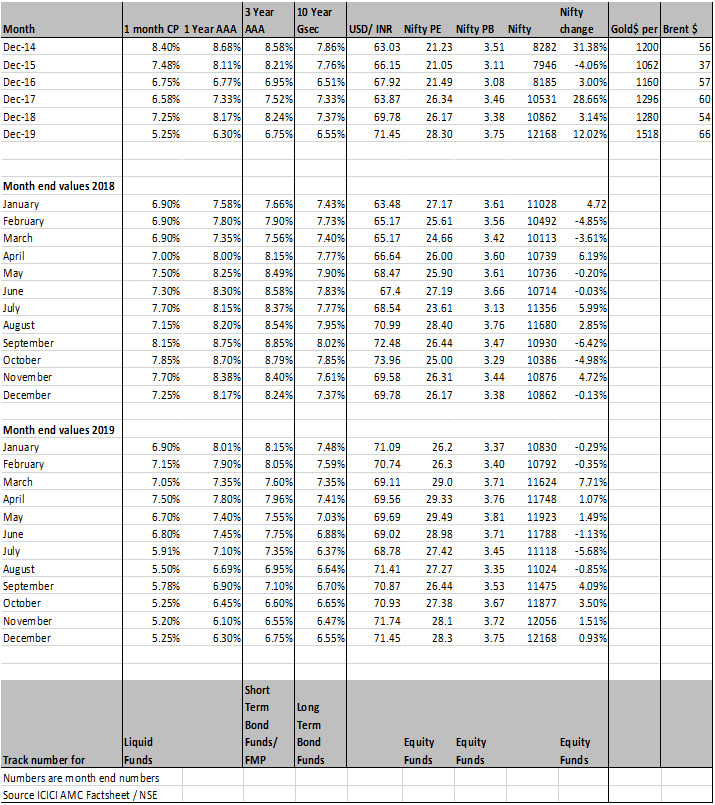

- Indian current account was under control at 2.3% while forex reserves hit a all time high of $450bn.

- Global markets displayed significant risk on behaviour.

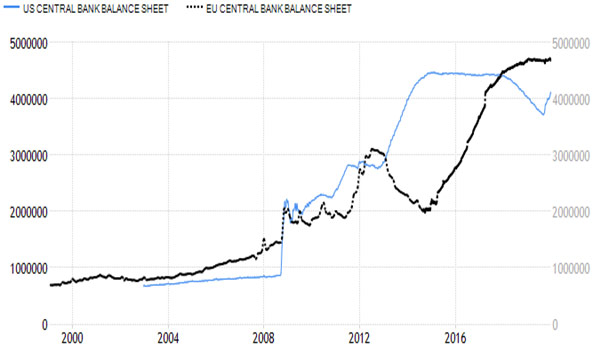

- US Fed reversed the rate hike cycle and also provided liquidity to the markets

- US Fed resumed expanding its balance sheet to provide sufficient liquidity to the markets

2. Our view on market behaviour in 2019

- US Fed rate cut and expectations of recovery has led to significant rally in global markets.

- In India earnings growth has been muted with the slowdown in GDP. However, post tax returns for alternatives has shrunk with drop-in interest rates and increase in tax rates for debt. This has resulted in chase for select few quality stocks.

- There has been a question that has crossed the minds of most investors on reasons for equity market not correlating with the slowdown in broader economy. One needs to dissect the same for better understanding. The broader market has not been reflecting performances which headline indices have witnessed. Therefore, while the actual correlation has been there, it has been camouflaged by the performance of select micro segments that have different drivers.

- The bank balance sheet clean- up is expected to gather momentum as the supreme court decided in November 19 favouring committee of creditors against the National Company Law Tribunal and primacy of financial creditors. The government has been nimble in exempting fresh buyers in insolvency proceedings from investigative agency actions for acts of previous owners.

- The government has also infused significant amount of capital into public sector banks.

- RBI has turned dovish after a long period of hawkish behaviour.

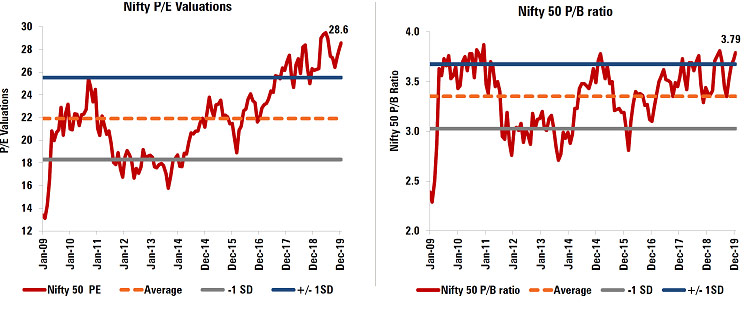

- The equity market valuations are at a high compared to historic averages. However, the earning cycle is yet to kick in. Markets have been willing to pay a premium to counters where earning visibility is strong.

3. Positives and negatives that await 2020

4. Positioning Portfolios

- Fixed Income investors can position portfolios towards maturities of three years. This helps obtain higher carry at 3-year maturity and not maintain any mismatch between when they can be liquidated with long term capital gains.

- Investors with risk appetite and very long- time horizons can take exposures to long end.

- We believe credit as a theme can be looked at very selectively. It is not clear if the delinquency cycle is behind us.

- We expect a positive 2020 for equity markets. Our hypothesis comes from the view that the slowdown is close to its bottom and global growth cycle is expected to pick up.

- We will continue to be selective in the mandates chosen as well as manager selection. This is primarily due to low visibility for very broad- based rally.

- We are yet biased towards large caps though valuation comfort exists on mid and small cap. We would like to look at mid-caps only selectively and prefer allocation to mutli-cap strategies, with discretion to the manager.

- Index investing has rationale post the very mandated nature of stock universe for schemes based on SEBI regulations.

- Manager selection can make a large difference given the significant gaps in performances over a cycle. As the general saying “the winner takes it all.” also applies to investing with managers who can navigate the cycles effectively.

- We believe that diversification is essential in portfolios. Two key diversification strategies that we advocate is asset allocation and geographic diversification.

- We have seen investors paying large attention to asset allocation but not so much importance to geographic diversification due to strong home country bias.

- We believe that diversification on assets that are not INR denominated needs to evolve given the ups and downs of macros that India has been witnessing in the past.

- Hence, we would advocate investors to gradually incorporate the same into portfolio asset allocations.

- Global growth and trade cycle.

- Geopolitics/ Oil prices impacting the Indian macros adversely.

- Resolution of stress asset problems plaguing the Indian banking system and a fresh cycle of growth.

- Improving earnings and return ratios for corporate India.

- Reform momentum includes disinvestments, fiscal adjustments, pushing forward domestic growth drivers, etc.

All graphs in the note has been sourced from ICICI AMC outlook 2020, IDFC AMC, websites and ACE MF Database. The note has been prepared and updated as of 03 Jan 20.

This publication has been issued by Trufid Wealth Management Private Limited for the information of its customers only.

This publication does not constitute investment advice or an offer to sell, or a solicitation of an offer to purchase or subscribe to any investment.

The information herein is derived from publicly available sources that Trufid considers reliable but which has not been independently verified.

Whilst every care has been taken in compiling the information, Trufid makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of Trufid only and are subject to change without notice.

Opinions expressed herein do not have any regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this publication.

Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies that may have been discussed in this publication and should understand that the views regarding future prospects may or may not be realized.

The information contained herein is confidential to the recipients thereof and may not be reproduced or otherwise disseminated.

Trufid or its officers, directors, or employees may have investments in any of the products such in this publication (or in any related products) and from time to time may add or dispose off any investment.

For private circulation only. The information contained herein is confidential to the recipients thereof and may not be reproduced or otherwise disseminated. .