Yes. This is meaningful due to the tax deferral.

To illustrate this, would like to show how the same impacts debt products as the tax on debt instruments such as deposits or interest paying securities is 30% and has to be paid each year.

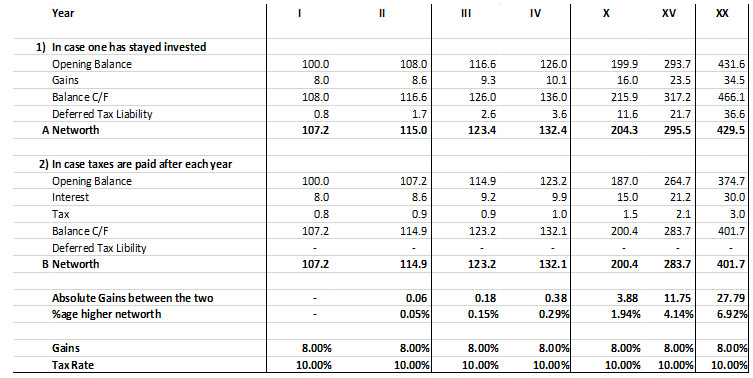

The following table provides a snapshot of how the numbers play out as we increase time horizons

The above working has used constant rate of 8% of gains and 30% tax on both the products to show the gains that arise out of deferring the tax liability.

In this table one can see how the deferred tax liability moves up from 2.4 to 34 in 10 years and 109 in 20 years. The progressive snowball is very large over longer periods of time.

One can also see the difference in net worth due to deferring the taxes v/s paying the same immediately. The net worth is higher by 5% in a 10- year period and 20 % over a 20 -year period.

One also needs to be mindful that the absolute amounts can be very significant given the %ages are that of the very high end values .

Debt Mutual Funds are the biggest area of opportunity as the gains are multi fold. Besides the tax liability getting deferred one gets a lower rate of taxation in debt funds.

The long- term tax rate on debt funds are 20 % post indexation which is estimated to be 10% -12% effective rate of tax as against the 30% tax on interest income

The table below shows how the same works out over longer periods of time

In this case the gains accrue on both the tax rate as well as tax deferral. One can see the %age net worth is higher by 17% in year 10 and 42% in year 20.

The absolute gain over a Rs 100 invested in the beginning is Rs 172 in year 10 and Rs 297 in year 20 which is quite significant.

Yes. the principle works in all cases. However, the gains will be significant only over longer horizons. To make things simple tax rate is taken as 10% for both debt and equity investments.

In this case one can see the difference in net worth is 2% in 10- Years and 7% over a 20- year period. The absolute numbers is Rs 4 for every 100 invested at the end of 10 years and 28 for every Rs 100 invested at the end of 20 years.

Yes. These are primarily to ensure increased tenure of holdings

1. Well defined objectives while structuring of portfolios to ensure longer shelf life

2. Structure the portfolio into Core/ Strategic and Non- Core/ Tactical to ensure there is limited rebalancing.

Select products that have a long shelf life where the investment objectives are unlikely to change and match with what is desired from the portfolio. (eg. Index Allocations, High Credit quality debt funds, clearly defining on risk tolerance in allocations, factoring in net yield post delinquencies for credit funds, risk versus rewards analysis etc).

1. Ensure the costs to the product are reasonable.

2. Traditional funds have a significant longer shelf life when compared to the flavour of the season investing.