Asset Allocations and Strategy

We have been hit with a health crisis which most of us have never seen before.

While 2008 crisis was a financial crisis which had only impact of one segment (Financial System). The fears then were that the financial crisis will seep and impact the normal lives of people and the real economy.

The current healthcare crisis due to Covid is one where the impact is directly on the lives of people and the real economy. This also seeps into the financial system given the costs to lockdown and the changing economic scenarios and way of doing business.

This raises many challenges for individuals and the system alike as

- Uncertainty has increased manifold

- One can extrapolate many models for human impact and financial impact to project the direction of the crisis. However, these primarily remain on paper as no one has a better idea of the timeline or how the same will change the way in which world works.

- Policy makers will use and try all arsenals in their domain to smoothen or reduce the damages to the system though each of them has unintended consequences which are not controllable

- The crisis will pass however one thing is certain it will throw out a different set of equation in terms of winners and losers and movement of economic actors.

Yields have come off significantly over the last one year. The RBI was on a rate cut cycle which got further accelerated due to the Covid crisis. This led to the near- term money rates coming off by 3% as against the RBI rate cuts of 1.75% over the last one year. The longer end of the curve has also seen the downward trajectory. The steepness of the near- term rates compared to long term rates is high. A tabulation of the yields across different durations are as below

Equity Markets

BSE Sensex moved from 27000 in 2015 to a high of 42000 in Jan 20. The index corrected sharply as it got to price in theCovid crisis and moved to a low of 25981 as on 23 March 20. The index has since recovered over the last two months to 34000 as on date. However, there has been sharp divergences in recoveries of individual stocks. The largest recovery has been in consumer names and Reliance which moved to a leadership given the monetisation of the telecom subsidiary.

International gold prices have been on an uptrend ever since the US Fed started reducing rates in 2019 and subsequently increasing its balance sheet size. The movement has further accelerated post the Covid crisis in March due to uncertainty and large amounts of monetary stimulus by various central banks.

While the frontline index is holding up there is significant gaps in individual portfolios based on the constituents and exposures to various sectors. This will continue to grow as we go forward.

It becomes difficult to actually quantify the real loss of economic value within different segments of the economy as the following is yet to be fully reflected. i.e.

- The financial sector losses camouflaged by the moratorium and deferral of standard asset class recognition.

- The numbers for the lockdown period are yet to be reported

- The actual break- even price and fresh price and volume levels based on the new norms to be followed for Covid

Given the nature of the crisis there has been significant levels of monetary stimulus provided by Central banks. The Government finances also are under stress given the revenue numbers will be significantly lower while expenditures are required to be carried out to cushion both economy and weaker sections of society.

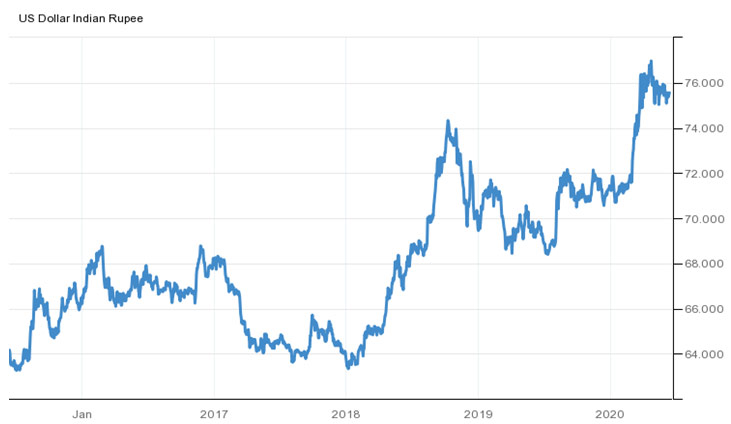

While there is no debate that this is the need of the hour and rightly instituted. Such measures over time can lead to financial system instability. In simple words whenever in an Indian scenario there has been imbalances on government spending and printing of money, we have had high levels of inflation and spurts of rupee depreciation. This cannot be underestimated.

This is a factor that investors have to very mindful about during a crisis scenario. This will be from the fact that some portions of the economy will never come back to the old normal and patterns of income and expenditure as the economy shifts.

In simpler words the current trend of technology replacing labour or higher work from home or lower social gatherings changes the nature of business activities pre and post covid. This can change the gainers or losers among economic agents and accordingly one needs to be highly alert to the same.

There is steepness in the yield curve besides a large gap between AAA and non AAA securities given that investors have risk aversion as well as uncertainty. We believe that the RBI has left some room for further rate cuts which will be used to push rates lower provided that there are no adverse external account shocks. In simple words there will be gravitational lower rates provided that the foreign investors do not liquidate their holdings or there is a high level of demand for imported products impacting the balance of trade.

Our view would be to focus purely on AAA assets with a mix of longer maturity roll down portfolio that forms core fixed income and the short maturities for ensuring liquidity as well as reducing the downsides for any adverse movements on interest rates.

Bucketing with higher focus on capital preservation would significantly aid in construction of the fixed income portfolios.

This is an asset class that one cannot avoid given that fixed income investments will not be able to match the purchasing power loss over time.

Our view on Indian indices is that they are holding up due to high level of liquidity infusion by Central Banks and lack of alternatives. However, there is a shift in the constituents with some segments severely beaten down.

We do not believe there will be a large- scale rally and prefer to be with larger names and more resilient segments of the economy compared to business which will need to be constantly supported to survive.

We will see a large number of zombie firms whose equity values will be traded on hope that these will come back if there is a large scale economic improvement. Hence, one would need to be selective in terms of allocations to fund managers or picking up direct investments to ensure that the segment provides the necessary kicker to the fixed income returns.

We would advocate to diversify equity holdings even geographically to ensure that there is exposure to firms that are a part of our expenditures while not being listed in the Indian equity markets.

This publication has been issued by TrufidWealth Management Private Limited for the information of its customers only.

This publication does not constitute investment advice or an offer to sell, or a solicitation of an offer to purchase or subscribe to any investment.

The information herein is derived from publicly available sources that Trufid considers reliable but which has not been independently verified.

Whilst every care has been taken in compiling the information, Trufid makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of Trufid only and are subject to change without notice.

Opinions expressed herein do not have any regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this publication.

Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies that may have been discussed in this publication and should understand that the views regarding future prospects may or may not be realized.

The information contained herein is confidential to the recipients thereof and may not be reproduced or otherwise disseminated.

Trufid or its officers, directors, or employees may have investments in any of the products such in this publication (or in any related products) and from time to time may add or dispose off any investment.

For private circulation only. The information contained herein is confidential to the recipients thereof and may not be reproduced or otherwise disseminated.